Navigating the Credit Card Maze After Buying a Car: When to Apply for Maximum Rewards

Congratulations! You just drove your shiny new car off the lot, a feeling that’s both exhilarating and liberating. But amidst the excitement, a thought pops into your head: wasn’t this the perfect time to snag a new credit card and rack up rewards points for future road trips? Should you slam on the brakes and wait, or hit “submit” on that application?

This dilemma plagues many car buyers. This blog post will be your roadmap, guiding you through the impact of car loans on your credit score and the pros and cons of applying for a new credit card right after your purchase. Ultimately, we’ll help you determine the best time to apply based on your specific credit goals.

Understanding How Car Loans Impact Your Credit Score

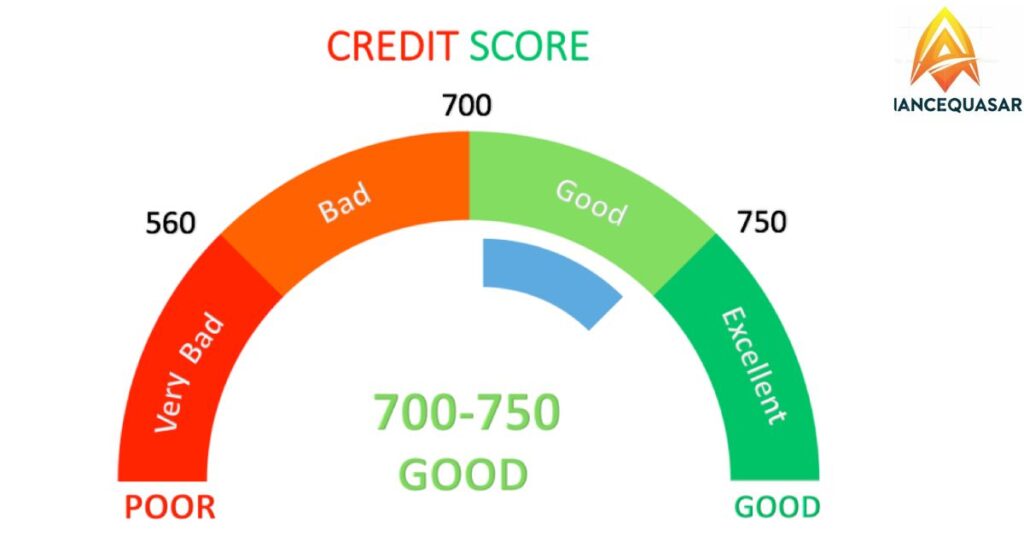

Before diving in, let’s revisit the credit score basics. Your credit score is a three-digit number that reflects your creditworthiness, essentially a grade lenders use to assess your ability to repay borrowed money. A higher score translates to a responsible borrower and typically qualifies you for better interest rates on loans and credit cards.

So, how does financing a car play into this equation? When you take out a car loan, the lender performs a hard inquiry on your credit report. This inquiry temporarily lowers your credit score by a few points, usually around 5-10. The reason? Multiple hard inquiries in a short period can signal to lenders that you might be overextending yourself financially.

The good news is this dip is temporary. As you make your car payments on time, your credit score will gradually recover.

Recoended post: What is the US CONNECT charge on bank statements?

Applying for New Credit Cards Temporarily Lowers Your Score (But There Can Be Advantages)

Now, let’s talk about applying for a new credit card after buying a car. Here’s the catch: applying for a new credit card also triggers a hard inquiry, which can cause another temporary dip in your credit score.

So, isn’t it best to just wait until your score fully recovers from the car loan inquiry before applying for anything else? Not necessarily. There can be some advantages to applying for a credit card strategically after buying a car.

Applying for a Credit Card After Buying a Car: Offers will Start Coming In

You might be surprised by the avalanche of pre-approved credit card offers flooding your mailbox after financing a car. This happens because lenders view responsible car ownership as a positive mark on your credit profile. They might see you as someone who can handle managing multiple credit lines responsibly.

Here’s the potential benefit.

If your credit score is healthy (generally above 670), applying for a new credit card shortly after your car purchase could allow you to capitalise on these pre-approval offers before your credit score fully reflects the car loan. This could land you a card with fantastic rewards programs, travel benefits, or introductory 0% APR periods on purchases.

Finding the Right Mix: Weighing the Pros and Cons

Of course, there’s another side to the coin. Here’s a breakdown of the advantages and disadvantages of applying for a new credit card after buying a car:

Advantages

- Capitalise on Pre-approved Offers: As mentioned earlier, you might snag a fantastic rewards card with a pre-approval offer.

- Potential Credit Score Boost: Managing multiple credit lines responsibly (paying your balances on time and in full) can actually improve your credit score in the long run.

- Build a Robust Credit History: Having a mix of credit products (instalment loans like car loans and revolving credit like credit cards) demonstrates your financial responsibility to lenders.

Disadvantages

- Multiple Hard Inquiries: Each new credit card application triggers a hard inquiry, which can further lower your credit score, especially if you apply for multiple cards in a short period.

- Temptation to Overspend: A new credit card with a high spending limit might be tempting, especially after a significant purchase like a car. Be mindful of your budget and avoid racking up debt.

Case Study: Sarah Navigates the Post-Car Purchase Credit Card Dilemma

Let’s look at a real-life example. Sarah just bought a new car and her credit score is a healthy 720. She’s bombarded with pre-approved credit card offers for travel rewards cards.

Option 1: Apply Now and Reap the Rewards

Sarah decides to take advantage of a pre-approved offer for a travel rewards card with a 0% introductory APR on purchases for 12 months. She plans to use the card for everyday purchases and pay the balance in full each month to avoid interest charges. This strategy allows her to earn valuable rewards points towards future trips while keeping her credit score healthy.

But There’s Another Way: Sarah Considers Waiting

Sarah isn’t sold just yet. While the travel rewards card is tempting, she’s also aware of the potential downsides. Here’s why Sarah might consider waiting a few months before applying for a new credit card:

Building a Stronger Credit Score Foundation

Remember, the car loan inquiry has caused a temporary dip in her score. Waiting 3-6 months allows her score to recover fully before applying for a new card. This could mean the difference between qualifying for a “good” vs. “excellent” tier card, with better rewards and interest rates.

Focusing on Responsible Credit Management

Sarah wants to solidify her responsible credit card use habits. By waiting and diligently making her car payments on time, she demonstrates her financial discipline to future lenders. This can be especially important if she’s planning other loan applications in the near future, like a mortgage.

Avoiding Overspending

Let’s face it, a new car purchase can be a financial strain. By waiting a few months, Sarah allows herself some breathing room to adjust to her new car payment and avoid the temptation to overspend on a new credit card, especially during the initial excitement of getting the card.

Deciding When to Apply: A Timeframe for Different Goals

So, when exactly should you apply for a new credit card after buying a car? The answer depends on your credit score and financial goals:

For Credit Score Optimization (Healthy Credit Score – Above 670)

- 3-6 Months: This time frame allows your credit score to recover from the car loan inquiry while offering a window to capitalise on pre-approved offers before they expire. You can leverage these offers to snag cards with the best rewards programs and

For Credit Building or Debt Repayment Focus (Lower Credit Score or History of Debt)

- 6-12 Months: This extended waiting period prioritises responsible credit card use and allows your credit score to solidify after the car loan inquiry. It also gives you time to focus on paying down any existing debt, which can significantly improve your creditworthiness.

Pro Tips for Applying for a Credit Card After a Car Purchase

Now that you have a roadmap for navigating the post-car purchase credit card application process, here are some pro tips to maximise your chances of getting approved for the best card:

- Shop Around: Don’t settle for the first pre-approved offer that lands in your mailbox. Research different cards and compare their rewards programs, annual fees, and interest rates to find the one that aligns best with your spending habits.

- Consider Pre-qualified Offers: Many issuers offer pre-qualification options that allow you to see if you’re likely to get approved for a card without triggering a hard inquiry. This is a fantastic way to explore different card options without harming your credit score.

- Focus on Responsible Credit Card Use: Regardless of when you apply, remember, the key to maximising your credit card benefits is responsible use. Pay your balances in full and on time to avoid interest charges and maintain a good credit score.

The Takeaway: Patience is Key

While the urge to snag a new credit card and start racking up rewards points might be strong, remember, patience is key! Waiting a few months after buying a car allows your credit score to recover from the car loan inquiry. This strategic approach can position you to land a card with the most lucrative rewards and benefits, ultimately putting you on the fast track to achieving your financial goals.

By following these tips and carefully considering your creditworthiness and financial goals, you can make an informed decision about applying for a new credit card after buying a car. Remember, responsible credit card use is the key to unlocking the true financial benefits these cards offer. Now, buckle up and get ready for a smooth ride towards credit card rewards and a healthier credit score!

Conclusion

Congratulations! You’ve navigated the exciting world of car buying and now you’re considering the strategic world of credit cards. While the temptation to snag a new card and start swiping might be strong, remember, a little patience can go a long way.

By waiting a strategic 3-6 months (for healthy credit scores) or 6-12 months (for lower scores or debt repayment focus), you allow your credit score to recover from the car loan inquiry.

This strategic approach can position you to land a card with the most lucrative rewards and benefits, ultimately putting you on the fast track to achieving your financial goals. So, buckle up, take a breath, and get ready for a smooth ride towards credit card rewards and a healthier credit score!

I am constantly seeking new challenges and opportunities to make a positive impact through my work. With my passion for innovation and drive for success, i continues to push the boundaries of what is possible in the ever-evolving world of technology.

In addition to my technical skills, I am known for my strong communication and leadership abilities. I thrives in collaborative environments, where i can leverage my expertise to drive projects forward and inspire teams to achieve their goals.