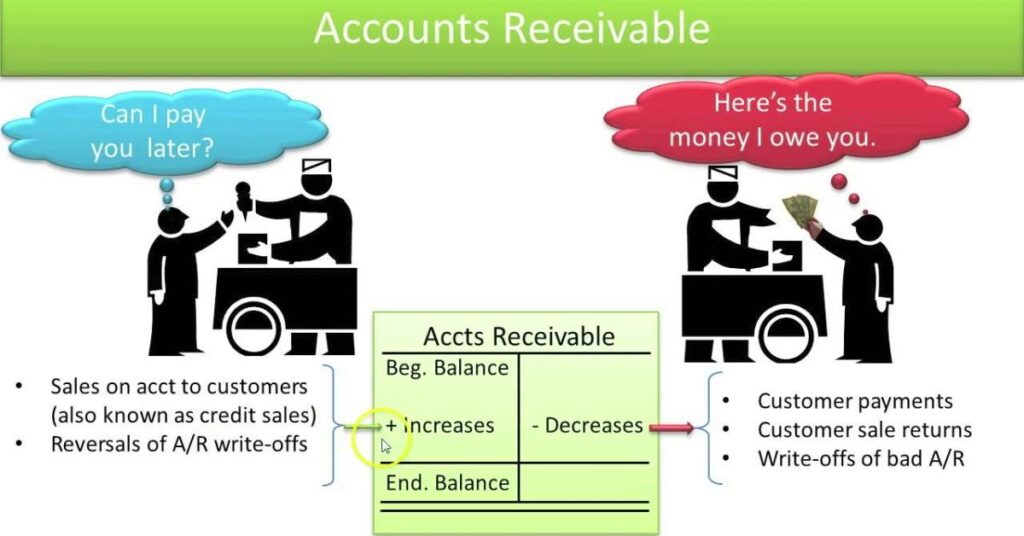

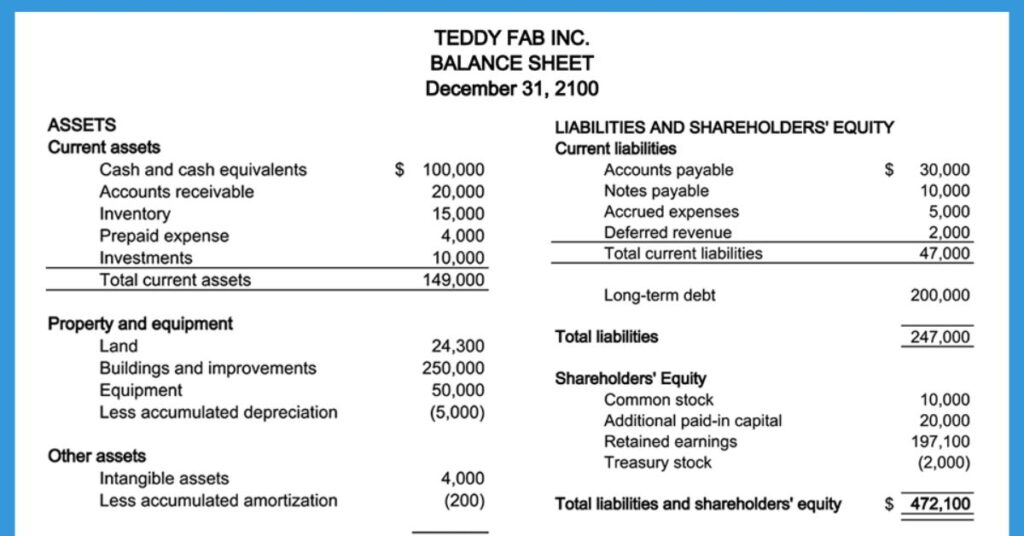

Accounts receivable is classified as a current asset on a company’s balance sheet. As a current asset, it represents the money owed to the company by its customers for goods or services that have been provided but not yet paid for. Current assets are those assets that are expected to be converted into cash within one year, making accounts receivable a vital component of a company’s short-term liquidity and financial health.

Curious about the financial backbone of businesses? Wondering why accounts receivable holds a pivotal role? Let’s delve into the intriguing world of finance and uncover the answer to the burning question: Is accounts receivable truly a current asset.

Accounts receivable is indeed classified as a current asset on a company’s balance sheet. As such, it represents the money owed by customers for products or services that have been provided but not yet paid for. This categorization as a current asset highlights its importance in assessing a company’s short-term liquidity and financial stability.

What are assets?

Assets are resources owned by a company that hold economic value and contribute to its financial well-being. In simple terms, assets are things that a company owns that can provide future benefits. These resources can be tangible, such as cash, inventory, equipment, and property, or intangible, such as patents, trademarks, and goodwill.

Assets are recorded on the company’s balance sheet and are categorised into current assets and noncurrent assets. Current assets are those that can be converted into cash or used up within one year, while non-current assets are those that are expected to provide benefits beyond one year. Assets play a crucial role in assessing a company’s financial health and determining its overall value.

What are Accounts Receivable Assets?

Assets are monetary amounts owed to a company by its customers or clients for goods sold or services rendered on credit. In essence, it represents the outstanding payments that the company expects to receive in the future. These assets are recorded on the balance sheet under the current assets section.

Accounts receivable assets are considered a vital component of a company’s financial health for several reasons:

1. Liquidity

While accounts receivable may not be immediately converted into cash, they represent funds that the company can reasonably expect to receive in the short term. This enhances the company’s liquidity position, allowing it to meet its immediate financial obligations.

2. Revenue Generation

Accounts receivable assets indicate revenue that has been earned by the company but not yet collected. As customers fulfil their payment obligations, these assets are converted into cash, thereby contributing to the company’s revenue stream

3. Cash Flow Management

Effective management of accounts receivable assets is essential for maintaining healthy cash flow. Timely collection of receivables ensures a steady influx of cash, which can be used to fund day-to-day operations, invest in growth opportunities, or repay debts.

4. Risk Management

Accounts receivable assets come with inherent risks, such as non-payment or delayed payment by customers. Companies must assess and mitigate these risks through measures such as credit checks, setting credit limits, and establishing provisions for doubtful debts.

5. Performance Evaluation

Monitoring the ageing of accounts receivable assets provides insights into the efficiency of the company’s credit and collection processes. It allows management to identify areas for improvement and implement strategies to expedite payment collection.

Is accounts receivable considered an asset?

Yes, accounts receivable is considered an asset. Accounts receivable refers to the money that a company is owed by its customers for goods or services that have been provided but not yet paid for. Since accounts receivable represent the right to receive cash in the future, they are classified as assets on the company’s balance sheet. As such, accounts receivable are included in the company’s total assets, reflecting the value of funds expected to be received from customers.

When are Accounts Receivable Assets Used?

Assets are used by companies in various ways throughout their operations. Here are some common scenarios when accounts receivable assets are utilised:

1. Sales Transactions

Accounts receivable assets are created when a company sells goods or services to customers on credit terms. Instead of receiving immediate payment, the company invoices the customer and records the amount owed as accounts receivable. This allows the company to facilitate sales transactions and extend credit to customers, thereby promoting sales and fostering customer relationships.

2. Cash Flow Management

Accounts receivable assets play a crucial role in managing cash flow. As customers fulfil their payment obligations, accounts receivable are converted into cash, which can then be used to cover operating expenses, invest in growth opportunities, or repay debts. By effectively managing accounts receivable, companies ensure a steady influx of cash to sustain their operations.

3. Revenue Recognition

Accounts receivable assets represent revenue that has been earned by the company but not yet collected. Revenue recognition principles dictate that revenue should be recognized when it is earned, regardless of when cash is received. Therefore, accounts receivable assets are used to recognize revenue in the accounting records, reflecting the value of goods or services provided to customers.

4. Credit Management

Companies use accounts receivable assets to manage credit risk and assess the creditworthiness of customers. By monitoring accounts receivable balances and ageing reports, companies can identify customers with overdue payments or those at risk of default. This enables them to take proactive measures, such as sending reminders, implementing credit controls, or negotiating repayment terms, to minimise bad debt losses.

5. Working Capital Management

Accounts receivable assets form part of a company’s working capital, which represents the funds available for day-to-day operations. By optimising accounts receivable turnover and reducing the average collection period, companies can enhance their working capital efficiency. This ensures that sufficient funds are available to support ongoing business activities and meet short-term financial obligations.

Recomended post: Seale et al. v. Altice USA, Inc. et al

Accounts receivable: asset, liability, or equity?

Accounts receivable is considered an asset, not a liability or equity. In financial terms, assets are resources owned by a company that have economic value and can be used to generate future benefits. Since accounts receivable represent money owed to the company by customers for goods or services provided, they are classified as assets on the balance sheet. Assets are things that a company owns and controls, which includes accounts receivable as they are expected to convert into cash in the future.

Is net accounts receivable a current asset?

Yes, net accounts receivable is typically considered a current asset. Current assets are assets that are expected to be converted into cash or used up within one year. Since net accounts receivable represent the amount of money expected to be collected from customers within a short period, usually within one year, they are categorised as current assets on the balance sheet.

Is accounts receivable revenue?

Whether accounts receivable is considered revenue depends on the accounting method used by the business. In cash basis accounting, revenue is recognized only when cash is received. Therefore, accounts receivable would not be considered revenue under this method because the cash has not been received yet.

However, in accrual basis accounting, revenue is recognized when a sale is made or when services are provided, regardless of whether cash has been received. In this case, accounts receivable represents revenue that has been earned but not yet collected. So, under accrual basis accounting, accounts receivable is considered revenue.

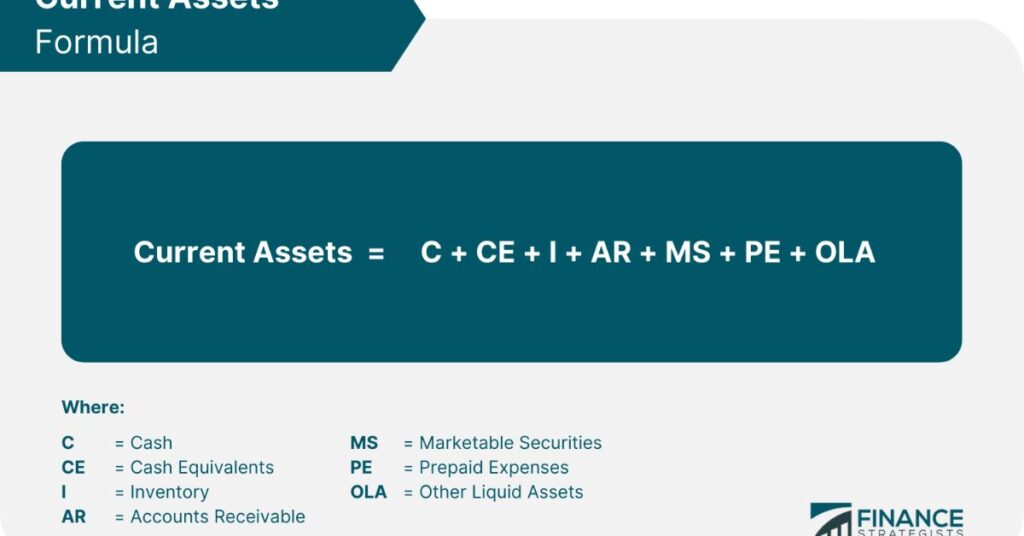

What are Current Assets?

Current assets are resources owned by a company that are expected to be converted into cash or used up within one year or the operating cycle, whichever is longer. These assets are easily liquidated and include cash, cash equivalents, accounts receivable, inventory, marketable securities, and prepaid expenses.

How to Calculate Current Assets

Calculating current assets involves summing up all the assets that meet the criteria of being convertible to cash or used up within the next year. The formula for calculating current assets is as follows:

Current Assets = Cash + Cash Equivalents + Accounts Receivable + Inventory + Marketable Securities + Prepaid Expenses + Other Liquid Assets

Examples of Current Assets

1. Cash: Includes physical currency, bank deposits, and petty cash.

2. Cash Equivalents: Short-term investments with high liquidity and low risk, such as Treasury bills and money market funds.

3. Accounts Receivable: Amounts owed to the company by customers for goods or services provided on credit.

4. Inventory: Raw materials, work-in-progress, or finished goods held for sale.

5. Marketable Securities: Investments that can be easily converted into cash, such as stocks and bonds.

6. Prepaid Expenses: Payments made in advance for goods or services, such as insurance premiums or rent.

7. Other Liquid Assets: Additional assets that can be quickly converted into cash, such as short-term loans receivable or prepaid taxes.

Significance of Current Assets

Current assets are a key indicator of a company’s short-term liquidity and financial stability. They provide valuable insights into the company’s ability to cover its short-term obligations, such as paying suppliers, servicing debt, and covering operating expenses. Current assets play a crucial role in financial analysis and decision-making, helping investors and creditors assess a company’s financial health and risk profile.

How to Treat Accounts Receivable on Your Books

Accounts receivable (AR) is a critical component of your company’s financial records, and how you handle it on your books can significantly impact your financial health and reporting accuracy. Here’s a guide on how to properly manage accounts receivable:

1. Recording Transactions

When you provide goods or services to customers on credit, you need to record the transaction in your accounting system. Debit the accounts receivable account to increase it, and credit the corresponding revenue account to recognize the sale.

2. Invoicing Customers

Issue invoices promptly to your customers for goods delivered or services rendered. Clearly state payment terms, such as due date and any applicable discounts for early payment.

3. Tracking Receivables

Maintain detailed records of all outstanding invoices and their status. Monitor aging reports to track the ageing of receivables and identify overdue accounts.

4. Reconciliation

Regularly reconcile your accounts receivable ledger with customer payments received. Ensure that all payments are properly applied to the corresponding invoices.

5. Allowance for Doubtful Accounts (AFDA)

Establish an allowance for doubtful accounts to account for potential non-payment by customers. This contra-asset account reduces the net value of accounts receivable to reflect the amount expected to be uncollectible.

6. Write-Offs

If a customer’s account becomes uncollectible, write off the bad debt by debiting the allowance for doubtful accounts and crediting accounts receivable. This removes the delinquent receivable from your books.

7. Collection Efforts

Implement effective collection procedures to minimise overdue accounts. Send reminders, make follow-up calls, and consider offering payment plans to encourage prompt payment.

8. Reporting

Include accounts receivable as a current asset on your balance sheet. Disclose any allowances for doubtful accounts and provide detailed disclosures in your financial statements.

9. Auditing

Regularly audit your accounts receivable processes to ensure accuracy and compliance with accounting standards. Address any discrepancies or weaknesses in internal controls promptly.

Accounts receivable is much more than an asset on your balance sheet

1.Accounts Receivable: Beyond a Balance Sheet Asset

Accounts receivable (AR) is not just a line item on your balance sheet; it serves as a vital indicator of your company’s financial health and operational efficiency. Here’s why AR is more than just an asset.

1. Cash Flow Management

AR represents the money owed to your business by customers for goods or services provided on credit. Effectively managing AR ensures a steady inflow of cash, supporting day-to-day operations and financial stability.

2. Customer Relationships

Timely and accurate invoicing, along with efficient AR processes, contribute to positive customer experiences. Clear communication and resolution of billing issues strengthen trust and foster long-term relationships with clients.

3. Risk Management

Monitoring AR ageing reports helps identify potential liquidity risks and overdue accounts. Prompt action can be taken to mitigate bad debt losses and minimise the impact on profitability.

4. Operational Efficiency

Streamlined AR workflows reduce administrative burden and processing time. Automation of invoicing, payment reminders, and collections enhances efficiency and frees up resources for strategic initiatives.

5. Insightful Analytics

Analysing AR data provides valuable insights into sales performance, customer payment trends, and cash flow forecasting. This information informs strategic decision-making and business planning.

6. Financial Reporting

Accurate recording and reporting of AR transactions ensure compliance with accounting standards and regulatory requirements. Transparent disclosure of AR balances and allowances enhances transparency and investor confidence.

2. Accounts Receivable: Mitigating Cash and Working Capital Uncertainty

Accounts receivable (AR) plays a crucial role in reducing uncertainty surrounding cash flow and working capital levels for businesses. Here’s how:

Stabilising Cash Flow

AR represents revenue that has been earned but not yet received in cash. By extending credit terms to customers, businesses can generate sales and revenue without immediate cash payments. This steady stream of AR helps maintain consistent cash flow, ensuring that operational expenses can be met and investments made.

Supporting Working Capital

Working capital, which is the difference between current assets and current liabilities, is essential for covering day-to-day operational expenses. AR contributes to working capital by representing funds that will be converted into cash within a relatively short period. This liquidity cushion allows businesses to manage inventory, pay suppliers, and fund growth initiatives without relying solely on external financing.

Forecasting and Planning

AR ageing reports provide insights into the timing of expected cash inflows from customers. By analyzing the ageing of receivables, businesses can forecast future cash receipts more accurately and plan accordingly. This visibility into future cash flows enables proactive management of working capital requirements and reduces the risk of cash shortages.

Minimising Financial Risk

Effective AR management involves assessing the creditworthiness of customers and implementing credit policies to mitigate the risk of non-payment or late payment. By conducting credit checks, setting appropriate credit limits, and monitoring payment behaviour, businesses can minimise the impact of bad debts and collection delays on cash flow and working capital.

Accounts receivable serves as a financial resource that enables businesses to maintain liquidity, manage working capital effectively, and navigate cash flow fluctuations with greater certainty and confidence. By optimising AR processes and monitoring receivables closely, businesses can enhance their financial resilience and operational stability.

3. Strengthening Customer Relationships through Accounts Receivable

Accounts receivable (AR) management goes beyond financial transactions; it plays a pivotal role in fostering stronger relationships with customers. Here’s how AR contributes to building lasting connections:

Transparent Communication

AR processes provide an avenue for transparent communication between businesses and their customers regarding payment terms, invoicing details, and outstanding balances. By maintaining clear and consistent communication channels, businesses demonstrate their commitment to transparency and accountability, which fosters trust and strengthens the customer relationship.

Flexible Payment Options

Offering flexible payment options and terms tailored to customers’ needs can enhance satisfaction and loyalty. AR departments can work with customers to establish customised payment plans or negotiate favourable terms, demonstrating a willingness to accommodate their preferences and financial circumstances. This flexibility can lead to improved customer satisfaction and long-term loyalty.

Timely Issue Resolution

Efficient AR management enables businesses to address billing discrepancies, payment disputes, and other issues promptly and professionally. By resolving issues in a timely manner and providing satisfactory solutions, businesses demonstrate their commitment to customer satisfaction and reinforce their reputation for reliability and responsiveness.

Personalised Engagement

AR personnel have direct interactions with customers during the invoicing and payment process. These interactions present opportunities to personalise the customer experience by addressing customers by name, offering personalised assistance, and expressing appreciation for their business. Personalised engagement fosters a sense of connection and loyalty, strengthening the bond between the business and its customers.

Value-added Services

AR departments can go beyond transactional interactions to offer value-added services that benefit customers. For example, providing access to online payment portals, offering educational resources on financial management, or delivering proactive reminders about upcoming payments can enhance the overall customer experience and demonstrate the business’s commitment to supporting its customers’ success.

By leveraging accounts receivable as a strategic tool for building stronger customer relationships, businesses can differentiate themselves in the marketplace, drive customer loyalty, and create advocates who are more likely to recommend their products or services to others.

4. Accounts Receivable Minimises Collection Costs

Efficient management of accounts receivable (AR) not only streamlines cash flow but also plays a significant role in reducing collection costs for businesses. Here’s how effective AR practices contribute to cost savings:

Streamlined Processes

Implementing streamlined AR processes, such as automated invoicing, payment reminders, and reconciliation procedures, reduces the time and resources required to manage outstanding receivables.

By automating repetitive tasks and minimising manual intervention, businesses can achieve greater efficiency in their collections operations, leading to cost savings associated with labour and administrative overhead.

Early Payment Incentives

Offering incentives for early payment, such as discounts or preferential terms, encourages customers to settle their accounts promptly. By incentivizing timely payments, businesses can accelerate cash inflows and minimise the need for prolonged collection efforts, thereby reducing associated costs like follow-up calls, dunning letters, and debt recovery services.

Proactive Communication

Maintaining proactive communication with customers regarding payment expectations, billing inquiries, and overdue accounts can help prevent payment delays and disputes.

Data-driven Decision-making

Leveraging data analytics and reporting tools to track key AR metrics, such as days sales outstanding (DSO), collection effectiveness index (CEI), and ageing receivables, enables businesses to identify trends, patterns, and areas for improvement in their collections processes.

By making informed decisions based on actionable insights, businesses can optimise their collections strategies, allocate resources more effectively, and reduce costs associated with inefficient or ineffective collection efforts.

Efficient Resource Allocation

Effective AR management allows businesses to allocate resources strategically to areas with the highest collection priority or potential for recovery.

By prioritising efforts based on factors such as customer creditworthiness, payment history, and invoice ageing, businesses can optimise resource allocation, minimise wasted effort on low-value accounts, and focus on maximising returns on their collections investments.

5.Critical Accounts Receivable Performance Metrics

Tracking key performance metrics is essential for evaluating the efficiency and effectiveness of accounts receivable (AR) management. Here are some critical metrics that businesses should monitor to assess their AR performance.

1. Days Sales Outstanding (DSO)

DSO measures the average number of days it takes for a company to collect payment after a sale is made. A lower DSO indicates faster collection of receivables, which can improve cash flow and liquidity.

2. Collection Effectiveness Index (CEI)

CEI evaluates the efficiency of the collections process by comparing the amount of cash collected during a specific period to the total amount of outstanding receivables. A higher CEI reflects a more effective collection effort.

3. Average Days Delinquent

This metric calculates the average number of days past due for invoices that are overdue. Monitoring average days delinquent helps identify trends in payment delays and assesses the effectiveness of collections strategies.

4. Percentage of High-Risk Accounts

Identifying high-risk accounts that are more likely to default on payments allows businesses to allocate resources appropriately and implement proactive measures to mitigate potential losses.

5. Bad Debt to Sales Ratio

The bad debt to sales ratio compares the amount of uncollectible receivables to total sales. A lower ratio indicates better credit management and a lower risk of bad debt write-offs.

6. Customer Payment Trends

Analysing payment patterns and trends for different customer segments helps identify potential issues, such as slow-paying customers or seasonal fluctuations, and tailor collections strategies accordingly.

7. Ageing Receivables Analysis

Segmenting receivables based on their age (e.g., current, 30 days past due, 60 days past due, etc.) provides insight into the ageing of outstanding invoices and helps prioritise collections efforts.

8. Percentage of On-Time Payments

Monitoring the percentage of invoices paid on time versus those paid late helps assess customer payment behaviour and identify opportunities for improvement in collections processes.

9. Cash Flow Impact

Analysing the impact of AR on cash flow and working capital levels helps evaluate the overall financial health of the business and identify areas for optimization in AR management.

10. Customer Satisfaction Metrics

While not directly related to financial performance, tracking customer satisfaction metrics, such as Net Promoter Score (NPS) or customer feedback, provides valuable insights into the effectiveness of AR processes in maintaining positive customer relationships.

6.Accounts Receivable: A Central Business Asset

Accounts receivable (AR) holds a pivotal role as a central business asset. Unlike physical assets such as property or equipment, AR represents the money owed to a company by its customers for goods or services already provided. Here’s why accounts receivable is considered a critical asset in the business landscape:

1. Liquidity

AR provides a source of liquidity for businesses, allowing them to convert outstanding invoices into cash flow. This liquidity is vital for meeting short-term financial obligations, funding operations, and supporting business growth.

2. Revenue Generation

AR reflects sales that have been made but not yet collected. As such, it represents potential revenue for the business. Timely collection of receivables enhances cash flow and contributes to the company’s bottom line.

3. Working Capital Management

Effective management of AR is essential for optimising working capital levels. By efficiently converting receivables into cash, businesses can maintain adequate liquidity to cover day-to-day expenses and pursue growth opportunities.

4. Customer Relationships

The AR process involves interactions with customers, from issuing invoices to collecting payments. Building strong customer relationships through transparent communication, timely invoicing, and efficient collections practices can enhance customer satisfaction and loyalty.

5. Credit Management

Assessing the creditworthiness of customers and establishing appropriate credit terms are integral aspects of AR management. By extending credit judiciously and monitoring payment behavior, businesses can minimise the risk of bad debts and payment defaults.

6. Cash Flow Forecasting

AR data provides valuable insights into future cash flow projections. By analysing receivables aging, payment trends, and collection efficiency, businesses can forecast cash flow more accurately and make informed financial decisions.

7. Financial Health Indicator

The level of accounts receivable relative to sales volume and industry benchmarks serves as a key indicator of a company’s financial health. High AR turnover ratios and low levels of delinquency suggest efficient operations and sound credit management practices.

8. Business Valuation

Accounts receivable is considered an asset on the balance sheet and contributes to the overall valuation of a business. Investors and stakeholders often assess the quality of AR and its impact on financial performance when evaluating the worth of a company. Effective management of AR is essential for sustaining business operations and driving long-term growth and profitability.

Current Assets vs. Non-Current Assets

In financial accounting, assets are categorised into two main groups: current assets and noncurrent assets.

Current Assets

Are assets that are expected to be converted into cash or used up within one year or one operating cycle, whichever is longer. These include cash, cash equivalents, accounts receivable, inventory, and prepaid expenses. Current assets are crucial for assessing a company’s short-term liquidity and its ability to meet its immediate financial obligations.

Non-Current Assets

Also known as long-term assets, are assets that are not expected to be converted into cash or used up within the next year. These include property, plant, and equipment (PP&E), intangible assets, long-term investments, and other assets with a useful life extending beyond one year. Non-current assets are important for evaluating a company’s long-term financial health and its ability to generate future income.

Types of Current Assets

1. Cash and Cash Equivalents

Cash and cash equivalents are highly liquid assets that can be readily converted into cash. This category includes physical currency, bank deposits, and short-term investments with maturities of three months or less. Examples of cash equivalents include Treasury bills, money market funds, and certificates of deposit (CDs).

2. Marketable Securities

Marketable securities are investments that can be easily bought or sold on the open market and converted into cash quickly. These securities include stocks, bonds, and mutual funds held by a company as part of its investment portfolio.

3. Accounts Receivable

Accounts receivable represent amounts owed to a company by its customers for goods sold or services rendered on credit. Accounts receivable are recorded on the balance sheet as a current asset and are typically expected to be collected within one year. They represent a claim against customers for payment and are an important component of a company’s working capital.

Does accounts receivable count as a tangible asset?

Yes, accounts receivable is considered a tangible asset. Tangible assets are physical assets that have a clear value and can be easily measured. While accounts receivable may not be physical in nature like machinery or equipment, they represent amounts owed to a company by its customers for goods or services provided. Since these amounts are legally obligated to be paid and have a measurable value, accounts receivable are classified as tangible assets on the balance sheet.

Accounts payable: Everything you need to know

Accounts payable is a crucial aspect of financial management for businesses. In this guide, we’ll cover everything you need to know about accounts payable, including its definition, importance, and how it impacts a company’s financial health.

What are Accounts Payable?

Accounts payable (AP) refers to the money a business owes to its suppliers or vendors for goods or services received on credit. It represents the company’s short-term liabilities, reflecting the amount it needs to pay to its creditors within a specified period, usually within 30 to 90 days.

Importance of Accounts Payable

Accounts payable plays a vital role in a company’s financial operations for several reasons:

1. Managing Cash Flow:

By keeping track of accounts payable, businesses can effectively manage their cash flow and ensure they have enough liquidity to meet their financial obligations.

2. Building Relationships with Suppliers:

Timely payment of accounts payable is essential for maintaining good relationships with suppliers. It enhances trust and credibility, often leading to better credit terms and discounts.

3. Financial Planning:

Accounts payable data provides insights into a company’s short-term financial obligations, enabling better financial planning and budgeting.

4. Compliance:

Adhering to payment terms and accurately recording accounts payable transactions ensures compliance with accounting standards and regulatory requirements.

5. Cost Savings:

Efficient accounts payable processes can help identify opportunities for cost savings, such as early payment discounts offered by suppliers.

Key Components of Accounts Payable:

Understanding the components of accounts payable is essential for effective management:

1. Invoice Processing:

This involves receiving invoices from suppliers, verifying the accuracy of the charges, and recording them in the accounting system.

2. Payment Processing:

Once invoices are approved, payments are processed based on agreed terms, such as net 30 or net 60 days.

3. Vendor Management:

Maintaining accurate vendor records and communicating effectively with suppliers is crucial for managing accounts payable efficiently.

4. Accruals and Adjustments:

Accrued expenses and adjustments are recorded to ensure that financial statements accurately reflect the company’s liabilities.

Accounts Payable Automation:

Many businesses leverage technology to streamline their accounts payable processes through automation. Accounts payable automation software helps reduce manual tasks, improve accuracy, and enhance efficiency in invoice processing, approval workflows, and payment scheduling.

FAQ’s

1. What is accounts receivable (AR)?

Accounts receivable refers to the money owed to a company by its customers for goods or services that have been delivered but not yet paid for.

2. Why is accounts receivable important?

AR is important because it represents a significant portion of a company’s assets and cash flow. Timely collection of receivables is crucial for maintaining liquidity and supporting ongoing business operations.

3. How do businesses manage accounts receivable?

Businesses manage accounts receivable by implementing effective invoicing processes, monitoring payment timelines, following up on overdue accounts, and maintaining communication with customers regarding payment terms.

4. What is the difference between accounts receivable and accounts payable?

Accounts receivable represents money owed to a company by its customers, while accounts payable refers to money owed by a company to its suppliers or creditors.

5. What are the risks associated with accounts receivable?

Risks associated with accounts receivable include late or non-payment by customers, bad debt losses, cash flow disruptions, and potential strain on relationships with customers.

6. How do businesses assess the creditworthiness of customers?

Businesses assess the creditworthiness of customers by conducting credit checks, reviewing payment history, analysing financial statements, and establishing credit limits based on risk tolerance.

7. What strategies can businesses use to improve accounts receivable turnover?

Strategies to improve accounts receivable turnover include offering discounts for early payment, implementing stricter credit policies, streamlining invoicing and collections processes, and using automated AR management systems.

8. What is the impact of accounts receivable on financial statements?

Accounts receivable appears as an asset on the balance sheet, representing potential future cash inflows. Changes in AR levels affect cash flow, working capital, and profitability, which are reflected in the income statement and cash flow statement.

9. How can businesses reduce the risk of bad debts associated with accounts receivable?

Businesses can reduce the risk of bad debts by conducting thorough credit assessments, establishing clear payment terms, monitoring receivables ageing, promptly addressing overdue accounts, and implementing effective debt collection strategies.

10. What role does technology play in accounts receivable management?

Technology plays a crucial role in streamlining AR processes, improving efficiency, enhancing data accuracy, enabling real-time monitoring, and facilitating communication with customers regarding invoices and payments.

CONCLUSION

Accounts receivable (AR) stands as a vital component of a company’s financial health, representing the outstanding balances owed by customers for goods or services rendered. As a current asset, AR reflects the company’s short-term liquidity and ability to meet its obligations.

Effective management of AR is essential for maintaining cash flow, supporting ongoing operations, and fostering strong customer relationships. By implementing efficient invoicing, collection, and credit assessment processes, businesses can optimise their AR management and mitigate risks associated with bad debt.

Ultimately, prioritising effective AR management enables businesses to strengthen their financial position, minimise cash flow disruptions, and sustain long-term growth in a competitive market landscape.

I am constantly seeking new challenges and opportunities to make a positive impact through my work. With my passion for innovation and drive for success, i continues to push the boundaries of what is possible in the ever-evolving world of technology.

In addition to my technical skills, I am known for my strong communication and leadership abilities. I thrives in collaborative environments, where i can leverage my expertise to drive projects forward and inspire teams to achieve their goals.